What is CSRD, exactly?

The Corporate Sustainability Reporting Directive (CSRD, or Directive (EU) 2022/2464) is the EU law that turned sustainability reporting into a statutory obligation, replacing the older Non-Financial Reporting Directive (NFRD). This landmark regulation required mandatory ESG disclosure for approximately 50,000 companies doing business within the European Union.

The directive itself is solely a requirement for reporting. Another regulation, the European Sustainability Reporting Standards (ESRS), adopted as Delegated Regulation (EU) 2023/2772, is the rulebook that determines what, exactly, should be included in a company’s report, and how this information should be reported. It outlines twelve standards, comprising 1,144 data points derived from double materiality assessments, mandatory limited assurance, and a global standard for financial and digital reporting.

Since 2022, companies across the globe have been preparing to comply with the law (CSRD) and the reporting standards (ESRS). Then, in February 2025 and again in February 2026, major changes to both documents were published by the EU, throwing companies into confusion about who is still responsible for reporting and what is still required. These changes occurred in two parts, and are commonly referred to as the Stop-the-Clock Directive (EU 2025/794) and the Omnibus Content Directive (EU 2026/470).

Directives of Deregulation

Stop-the-Clock Directive (EU) 2025/794

Published 16 April 2025, this directive delayed Wave 2 reporting by two years to 2028 and FY2027, and Wave 3 reporting to 2029 and FY2028. It also pushed the transposition deadline for the Corporate Sustainability Due Diligence Directive (CSDDD), the directive requiring companies to assess and address human rights and environmental impacts across their supply chains, to 26 July 2027.

Omnibus – Content Directive

Proposed 26 February 2025 and adopted by Council 24 February 2026, this directive went into effect on 18 March 2026. It is a substantive deregulation. It redefined the scope and value-chain cap for companies required to participate in the CSRD, and furthermore, it withdrew certain sectoral standards and dropped the expectation of a “reasonable assurance pathway” altogether.

New Scope of CSRD

The CSRD now applies only to companies with more than 1,000 employees on average during the financial year and with more than a €450 million net annual profit.

This drastically changed the number of companies within scope for reporting, reducing the number from 50,000 to approximately 7,000 (a reduction of nearly 80%). The update applies for financial years beginning on or after Jan 2027, with the first reports due in 2028.

Key Differences after Omnibus

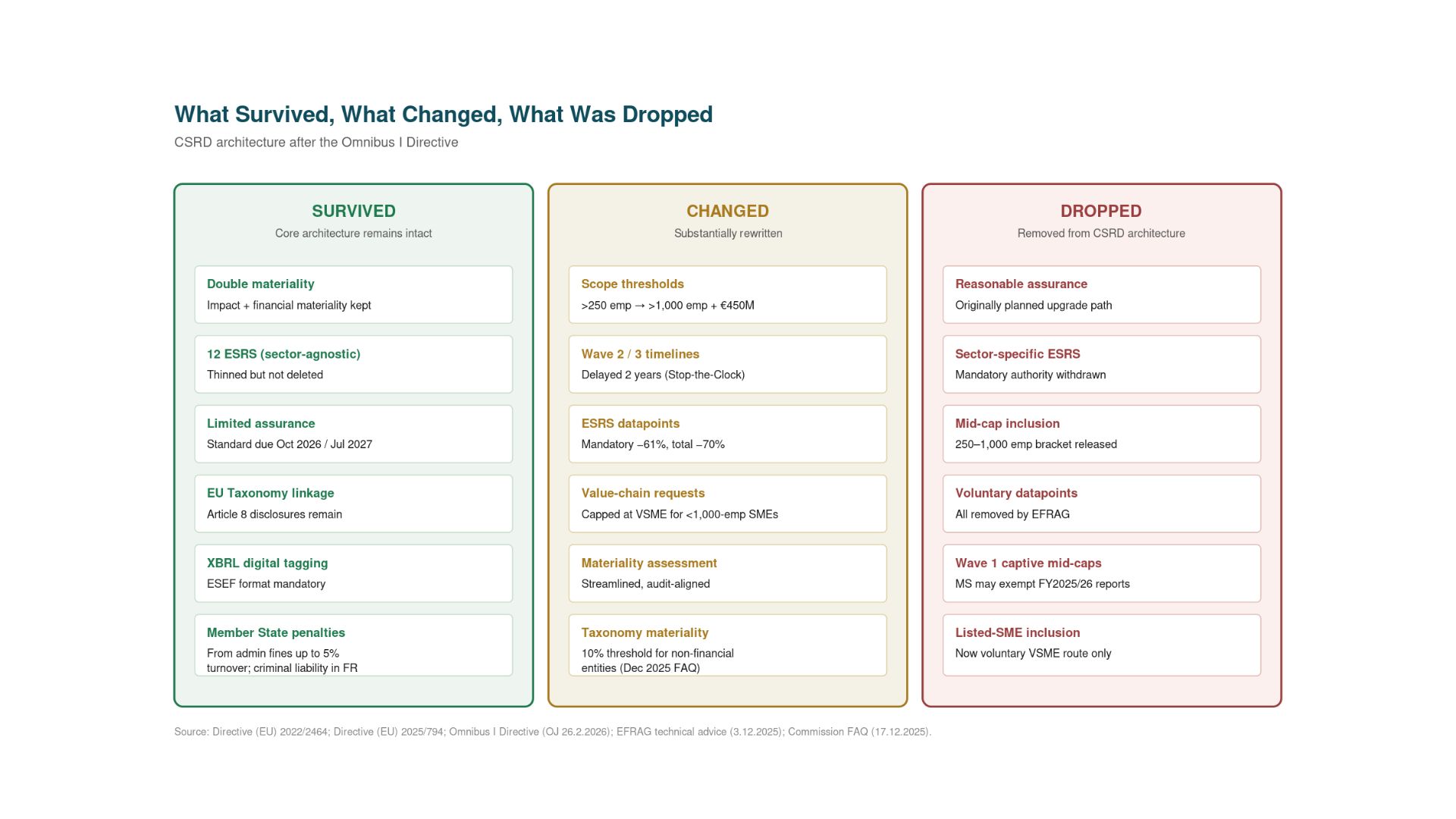

What Survived

The intention of the original CSRD is maintained by the core architecture that was not changed: double materiality, the 12 ESRS, Limited Assurance, EU Taxonomy Linkage, XBRL Digital Tagging, and Member State Penalties.

What Changed

The introduction of the Voluntary Sustainability Reporting Standard for Micro-Enterprises (VSME) represents a new shared baseline for data collection. Brand owners need data for Scope 3 emissions reporting, and packaging companies need carbon, water and material data for Life Cycle Assessment (LCA). But companies can no longer demand sustainability information beyond the VSME from value-chain partners with 1,000 or fewer employees. Micro-enterprises are entitled to refuse requests beyond the VSME.

What was Dropped

The European Financial Reporting Advisory Group (EFRAG) simplified the ESRS in technical advice delivered 3 December 2025. This advice cut mandatory data points by roughly 61% and removed all voluntary data points, totaling a reduction in data points of 70%.

Other items removed from the ESRS include reasonable assurance pathways, mandatory sectoral standards, and the inclusion of mid-cap enterprise requirements for reporting. The EU also adopted a new “usefulness and fair presentation” principle that gives companies more discretion to filter disclosures.

A common interpretation of these changes is reading “70% reduction” as “70% less work.” But the 30% of data points that remain are the ones with the highest time investment: climate inventory, transition plans, workforce and governance, taxonomy ratios, and the materiality narrative.

What’s Next?

Companies remaining in scope

While there is a two-year delay, companies should use this time to build the necessary data architecture for reporting, not as a reason to pause efforts in this direction. Additionally, companies must monitor the Commission’s final adoption of simplified ESRS in 2026.

Companies no longer in scope

For these companies, reporting obligations under CSRD may no longer apply, but sustainability data requests from investors, banks, ESG rating agencies, and large customers will continue. The VSME standard provides a structured framework for mid- and small-cap companies navigating these requests. Furthermore, the value-chain provision establishes the VSME-based voluntary standards as the legal limit on what information may be required from suppliers with 1,000 or fewer employees. Companies considered mid- and small-cap enterprises should take this extra time to familiarize themselves with the standard.

What do you need to be ready?

1 – A defensible double materiality assessment with quantitative evidence

2 – Audit-trailed GHG inventory across Scope 1, 2 and 3

3 – VSME-aligned supplier data collection respecting the value-chain cap

4 – Data point mapping to ESRS and ISSB, with XBRL tagging ready

The same dataset applies to CSRD, EU Taxonomy Article 8, PPWR eco-modulation, and the Digital Product Passport.

Explore Trayak for CSRD

If you are interested in learning more about how Trayak Consulting can assist you with these regulations, reach out to your Trayak contact or fill out our contact us form.