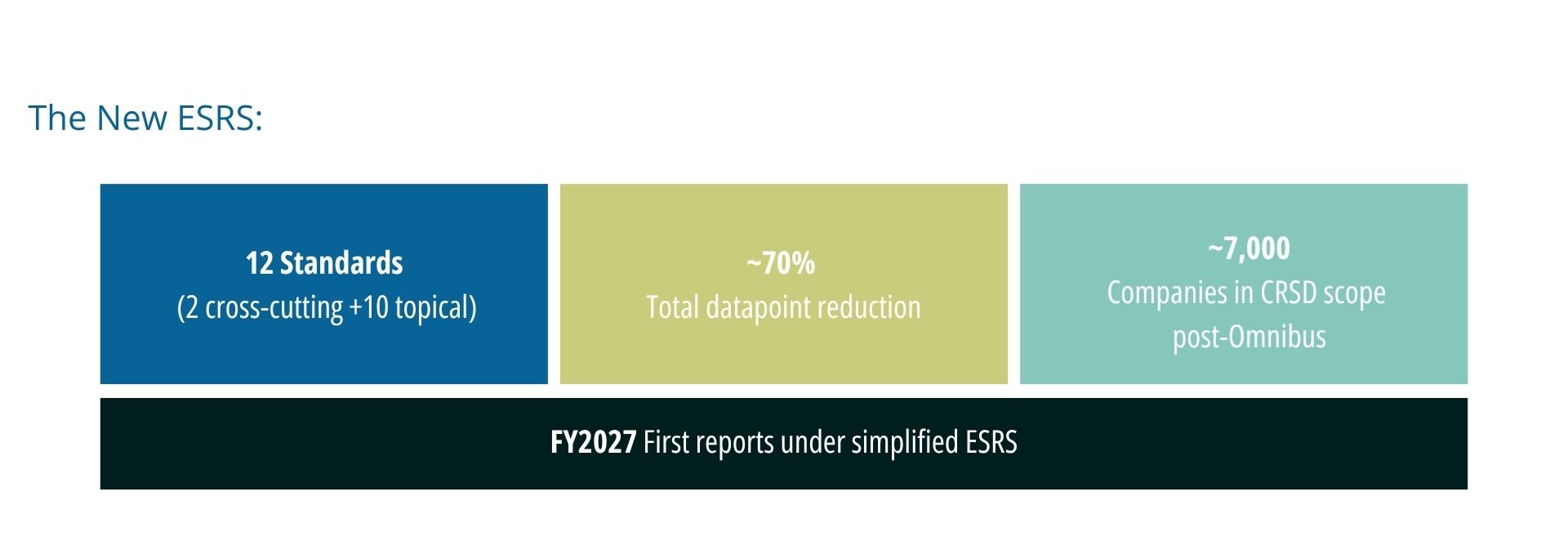

A year ago, preparing for CSRD meant preparing for ESRS – twelve standards, 84 disclosure requirements, and approximately 1,144 datapoints. Then, EFRAG delivered its simplification advice on December 3rd, 2025.

The simplified ESRS are expected to be adopted over the summer and to apply from financial year 2027, with voluntary early adoption from FY2026 permitted.

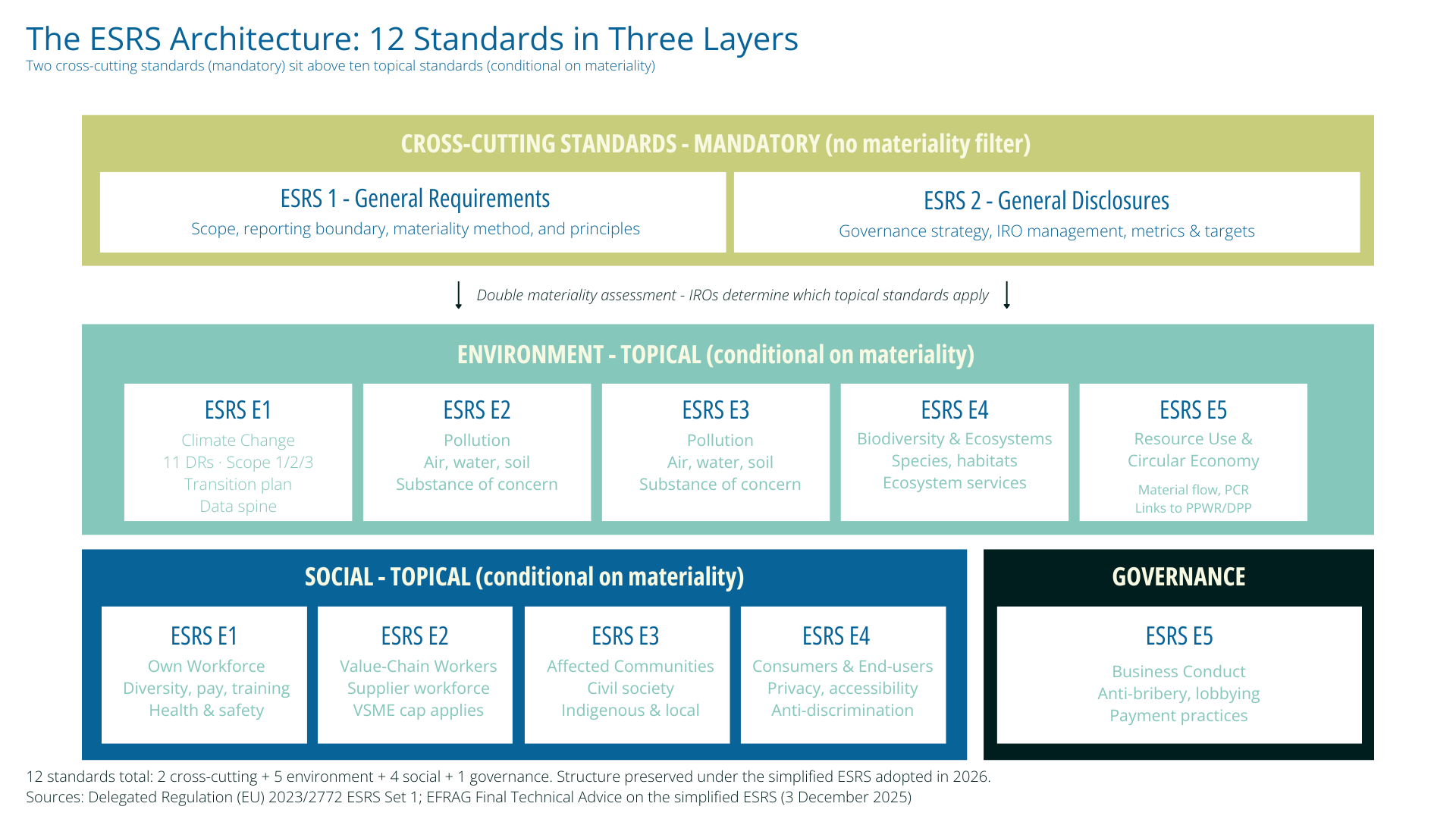

Figure 1: Changes to the 12 ESRS, made by the European Financial Reporting Advisory Group in 2025.

The 12 Standards

The ESRS – adopted as Commission Delegated Regulation (EU) 2023/2772 on 31 July 2023 – are 12 standards that make up the technical rulebook under the CSRD. They fall into 4 different categories: general, environmental, social, and governance.

Breakdown:

2 General:

ESRS 1 General Requirements and ESRS 2 General Disclosures apply to all companies.

5 Environmental:

E1 Climate Change, E2 Pollution, E3 Water and Marine Resources, E4 Biodiversity and Ecosystems, E5 Resource Use and Circular Economy

4 Social:

S1 Own Workforce, S2 Workers in the Value Chain, S3 Affected Communities, S4 Consumers and End-users

1 Governance:

G1 Business Conduct

The ten topical standards apply only if a topic is material to your business – through impact, financial risk, opportunity, or some combination of the three.

Figure 2. The ESRS architecture.

Double Materiality: Inside-out, Outside-in

Under the ESRS, a company has to assess two kinds of materiality at once. Impact materiality (effects on people and the environment, looking outwards) and financial materiality (effects of sustainability topics on the company’s financial position, looking inwards). Either assessment on its own is enough to make a topic disclosable. The Omnibus negotiations tried to drop this and move to single materiality, but the final text kept requirements for double materiality assessments intact.

The assessment is supported by IROs – impacts, risks and opportunities. The 2026 simplification streamlined the process: a business-model-based shortcut to clear-cut conclusions, sector-based opt-outs for non-material topics, a tier-1 supplier limit with safe harbours for reasonable estimates, and a new “usefulness and fair presentation” principle.

<Read about how Trayak can help you with the Double Materiality Assessment>

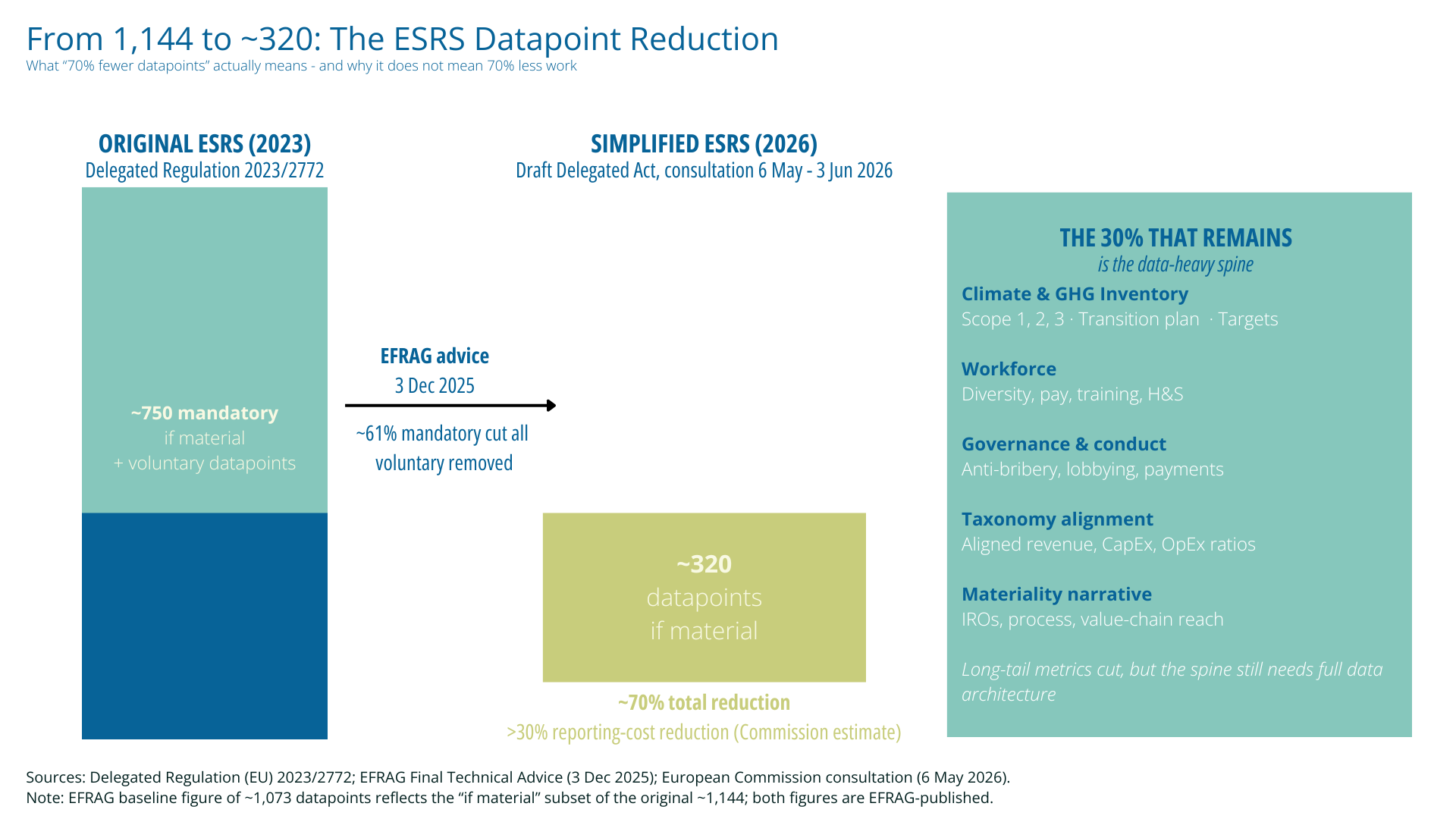

The Simplification in Numbers

EFRAG’s December 2025 technical advice cut mandatory data points by around 61%, removed all voluntary datapoints, and reduced the total to roughly 320 (if material) from about 1,073, a total reduction of 70%. The Commission’s impact assessment estimates a reporting cost reduction of more than 30% per company.

Figure 3. The Simplified ESRS

What survived: all twelve standards, double materiality, the IRO logic, ESRS 1 and 2 as mandatory rails, and ESRS E1 (Climate Change) as the data backbone. The amended ESRS E1 expands to eleven disclosure requirements – a 1.5°C-aligned transition plan, full Scope 1/2/3 GHG inventory, scenario analysis, a separate resilience disclosure, internal carbon pricing, GHG removals and carbon credits, and financed emissions for financial institutions.

A common interpretation of these changes is reading “70% reduction” as “70% less work.” But the 30% of data points that remain are the ones with the highest time investment: climate inventory, transition plans, workforce and governance, taxonomy ratios, and the materiality narrative. To learn more about changes to the CSRD after the Omnibus, read our blog.

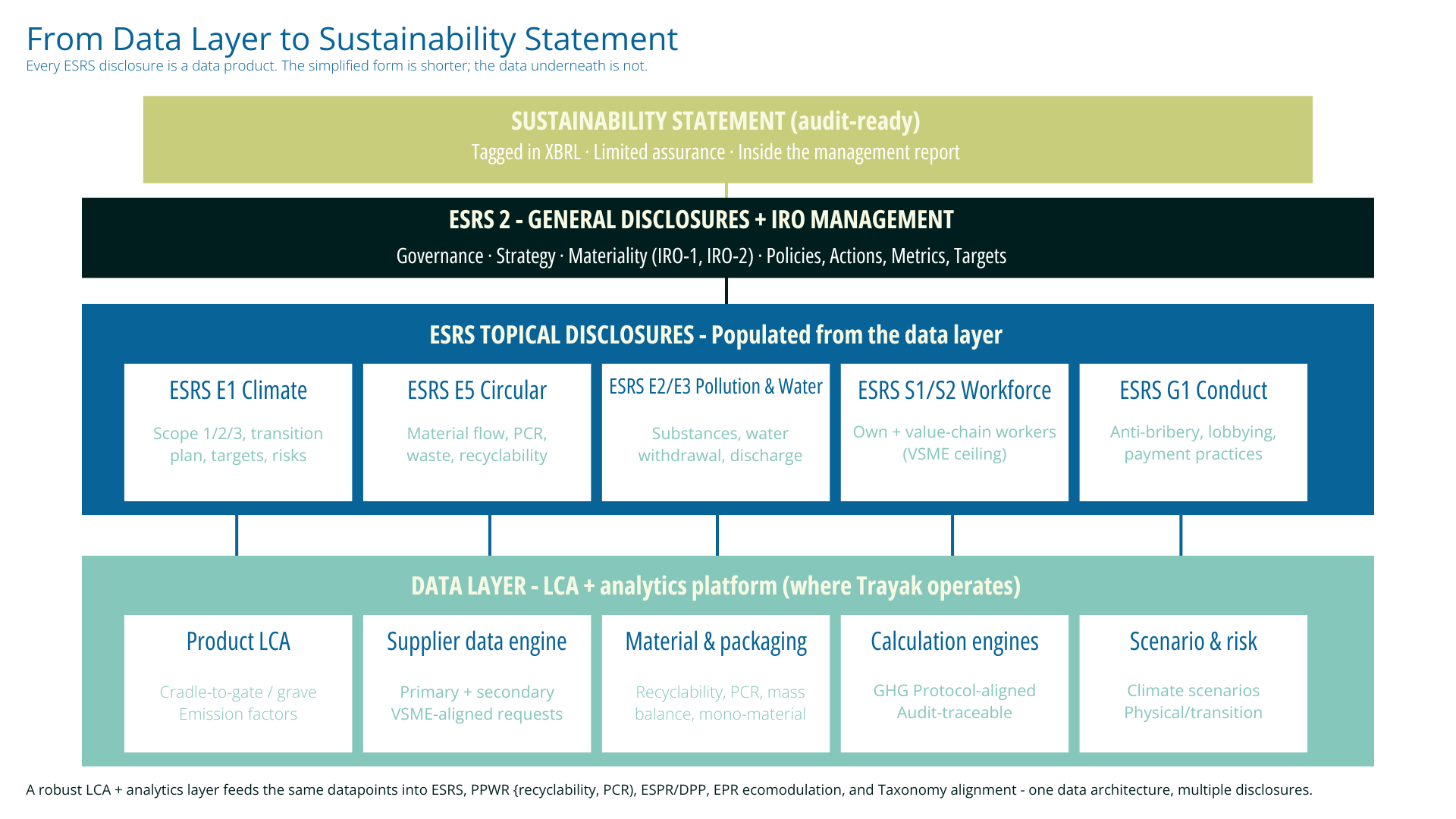

The Data Architecture Question

Every serious ESRS disclosure is a data product. ESRS E1 is a GHG and climate data product. ESRS E5 is a material-flow and product-lifecycle data product. ESRS E3 is a water-balance data product. ESRS 2 is a materiality-evidence data product. It is impossible to honestly disclose under the ESRS without the underlying numbers, and for any business of meaningful size, those numbers cannot be calculated in a spreadsheet.

Figure 4. A single data layer that to disclose and report for multiple standards.

This is where LCA-driven analytics platforms can help. Trayak’s EcoImpact platform exists for exactly this data: product-level lifecycle assessment that feeds Scope 3 emissions for E1, material flow and recyclability for E5, water and waste footprints for E3, and packaging analytics that connect directly to PPWR and the Digital Product Passport.

What Next?

If you are a Wave 1 reporter, you continue under the original ESRS in 2026 (on FY2025) and 2027 (on FY2026). Watch for formal adoption of the simplified version – voluntary early adoption from FY2026 may be available. If you are Wave 2 and remain above the new 1,000-employee, €450M Omnibus threshold, your first mandatory report is in 2028 on FY2027 data, under the simplified standards. Start the materiality assessment now and build the LCA dataset for your product portfolio. If you have fallen out of CSRD scope, the ESRS still matter to you. Customers, investors and lenders will ask for this information, and when they do, the most competitive companies will have already prepared a response.

React in Defense… or Plan an Offense?

The ESRS in 2026 are smaller in form than in 2023, but no less serious in substance. The data has to be defensible. The materiality has to be defensible. The transition plan has to be defensible. But if companies first build the data layer to support these disclosures, then they can disclose under ESRS, PPWR, DPP and EPR many times with confidence in their operations. The shorter form of the ESRS just means there is nowhere left to hide.

Get started with Trayak today

Trayak’s EcoImpact Sustainability Platform feeds product-level GHG, material flow, recyclability and supplier data directly into ESRS, PPWR, DPP and EPR workflows.

Published by Trayak. The data architecture section reflects Trayak’s commercial positioning as a provider of LCA and packaging analytics for ESRS, PPWR, DPP and EPR.